The AI Armor vs. The Yield Sword: Tech’s High-Stakes Balancing Act

Richard Smith

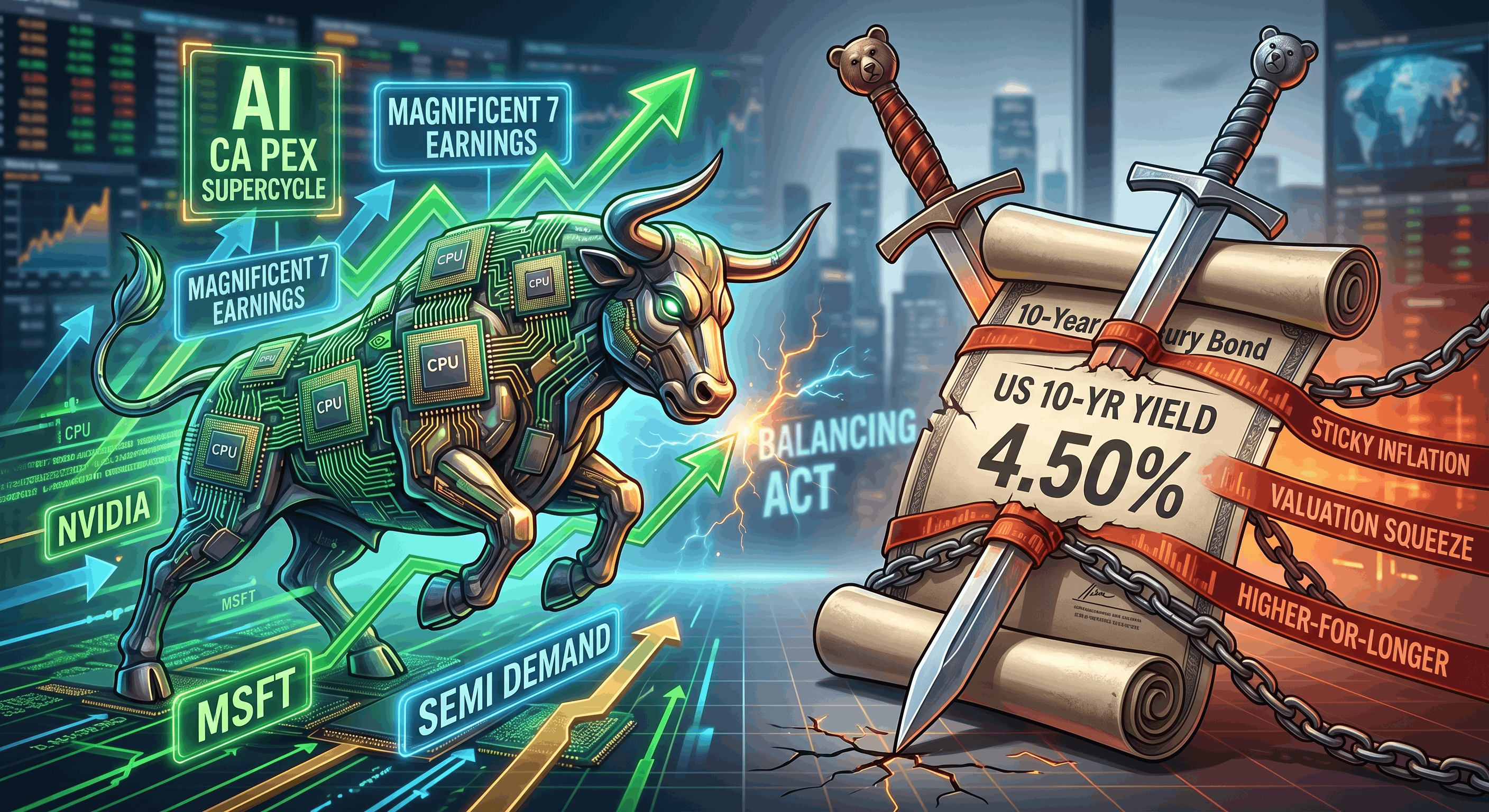

In the financial world, the current narrative is a tale of two competing forces: the indomitable momentum of Artificial Intelligence (AI) and the tightening grip of rising Treasury yields. For the "Magnificent 7" and their peers, the market has become a high-stakes arena where record-breaking earnings are fighting to stay ahead of a deteriorating bond market.

1. The Momentum: AI Infrastructure as a Macro "Shock Absorber"

The technology sector isn't just growing; it's undergoing a massive structural overhaul. Recent "blowout" earnings from key semiconductor players like Nvidia and TSMC have signaled that the AI investment cycle is accelerating rather than cooling.

Analysts have broadly upgraded the sector, shifting focus from "hype" to "hard infrastructure." We are seeing a "CapEx Supercycle" where spending on data centers and AI factories is providing a buffer against broader economic slowdowns.

The Shift: Leadership is broadening. While the original "Magnificent 7" (Apple, Microsoft, Alphabet, Amazon, Nvidia, Meta, and Tesla) dominated 2024 and 2025, the 2026 rally includes "second-tier" beneficiaries like chip-equipment makers and specialized cloud providers such as Oracle and CoreWeave.

+1

Earnings Visibility: Major players are securing multi-year contracts, with some infrastructure deals extending as far as 2032, providing the revenue certainty that high-valuation stocks desperately need.

2. The Pressure: The Yield Curve’s Shadow

The "Achilles' heel" of this tech-driven optimism is the U.S. Treasury Market. Yields are edging higher, with the 10-year Treasury recently fluctuating between 3.75% and 4.5%.

For tech stocks—often categorized as "long-duration assets"—higher yields are a direct threat. When the "risk-free rate" of a government bond rises, the present value of future corporate earnings drops. This makes "growth at any price" a dangerous strategy.

Valuation Sensitivity: Sentiment has soured slightly in the bond market due to persistent inflation (hovering near 3%) and a massive supply of government debt.

The Disconnect: While earnings remain strong, the "Magnificent 7" have recently seen their price-to-earnings (P/E) ratios compressed. Investors are no longer willing to pay a premium for growth if they can get a guaranteed 4%+ yield from Uncle Sam.

3. Markets Under the Microscope: Who is Affected?

The current tug-of-war between tech momentum and rate sensitivity is rippling across several key markets:

Market Segment | Impact Status | Why? |

|---|---|---|

Nasdaq 100 | Volatile | Heavily weighted with "rate-sensitive" names. It thrives on AI news but retreats sharply on "hotter-than-expected" inflation data. |

Fixed Income (Bonds) | Bearish | Rising yields mean falling bond prices. The 10-year Treasury is the focal point for all valuation models. |

Energy & Commodities | Bullish | Geopolitical jitters in Iran and Venezuela have kept oil near $100 per barrel, fueling the inflation that keeps yields high. |

Cloud & Semi-Sectors | Aggressive Growth | Names like Nvidia and Oracle are decoupling from the broader macro-woes due to unprecedented demand for GPUs. |

Export to Sheets

The Verdict: A "Show Me" Market

As we move further into Q2 2026, the era of "easy money" is a distant memory. The tech sector's survival as a market leader depends entirely on its ability to turn massive AI capital expenditures into tangible productivity gains.

If tech giants can prove that AI is significantly boosting their bottom lines, they may remain resilient even if Treasury yields stay "higher for longer." If the earnings start to slip, however, the "yield sword" may finally cut the rally short.

Journalist’s Note: Keep a close eye on the Federal Reserve’s next move. If they pause rate cuts due to "sticky" inflation, the valuation squeeze on the Magnificent 7 could intensify, regardless of how many chips Nvidia sells.