Market Alert: U.S. Inflation Surges to 3.8%, Higher Than Forecasted

Richard Smith

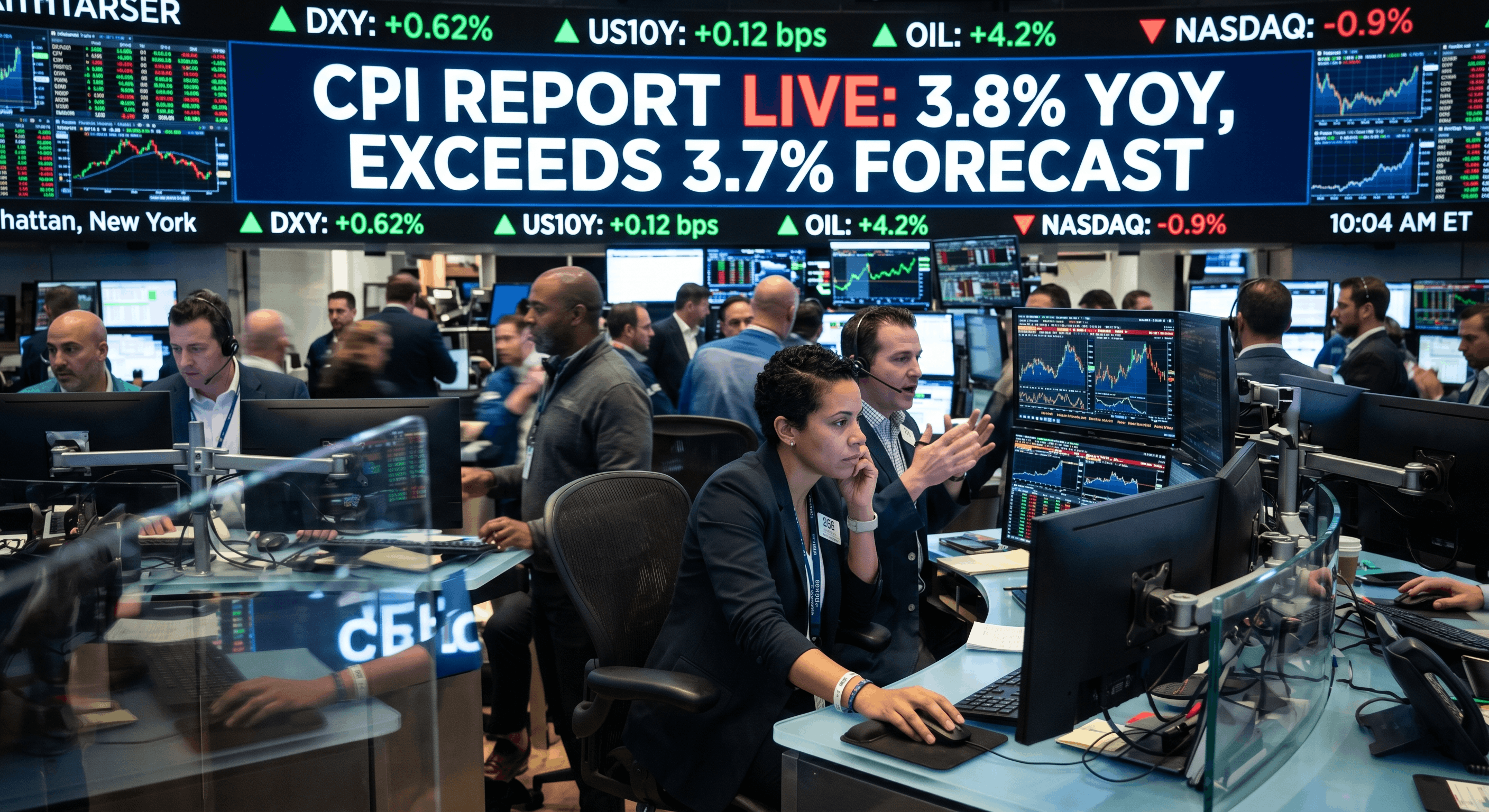

The Bureau of Labor Statistics (BLS) released the April Consumer Price Index (CPI) today, confirming market fears of broadening price pressures. Headline inflation jumped to 3.8% year-over-year, exceeding the 3.7% consensus and marking the highest level since mid-2023.

Key Data Breakdown

Headline CPI (YoY): 3.8% (Actual) vs. 3.7% (Forecast).

Core CPI (MoM): 0.4% (Actual) vs. 0.3% (Forecast).

Energy Sector: A massive 17.9% increase over the last 12 months, fueled primarily by the ongoing conflict in the Middle East and the subsequent oil supply shock.

Shelter & Services: Shelter prices rose 0.6% in April, while "supercore" services (excluding housing and energy) remained stubbornly high at 0.45% MoM.

Trader Outlook: The "Hot" Reading Impact

The hotter-than-expected print has immediate implications across three primary asset classes:

1. Currencies: The Dollar (DXY) Strengths

The uptick in Core CPI (0.4% MoM) reinforces the "higher-for-longer" interest rate narrative. Traders should expect the U.S. Dollar to catch a bid as yield differentials tilt in favor of the greenback. The 2.8% Core YoY reading suggests that even without energy volatility, underlying inflation is drifting away from the Fed's 2% target.

2. Fixed Income: Bond Yields Under Pressure

Treasury yields are expected to move higher as the market reprices the Federal Reserve’s "dot plot." With the June 16–17 FOMC meeting on the horizon, the probability of a rate cut has plummeted. Investors are now bracing for a more hawkish tone from incoming Fed Chair Kevin Warsh, despite political pressure for lower rates.

3. Equities: Pressure on Risk Assets

High-growth sectors and AI-driven equities, which have recently carried the market to record highs, may face a valuation squeeze. Rising yields increase the discount rate for future earnings, making expensive tech stocks more vulnerable to a pullback.

The Catalyst: Middle East Tension & Tariffs

Traders must account for two external "inflationary tailwinds" that appeared in the April data:

The Iran Shock: Brent crude remains volatile near $104/barrel, keeping gasoline and transportation costs elevated.

Tariff Transmission: Evidence suggests that trade levies and a 10% import tax under the Trade Act of 1974 are finally bleeding into core goods, ending the era of "goods deflation" that helped stabilize prices in 2025.

Trader’s Note: Keep a close eye on the 10-year Treasury yield. A break above key resistance levels following this report could signal a broader rotation out of equities and into defensive positions as the Fed's "inflation battle" enters a difficult new phase.